Bit Happens

Shifting Dynamics, Emerging Markets & Bitcoin’s Moment of Truth

Batten down the hatches, lock your bins and reach for the pepper spray because though it’s not yet Spring, bear season is upon us.

This was validated by three things that occurred throughout the past month. Firstly, crypto deity and market influencer Sam Bankman-Fried (CEO of FTX, a.k.a SBF) tweeted this:

Bitcoin was trading at ~US$43,000 at the time.

Then, market graphs started to look like this:

Finally came the last nail in the coffin, an unusually voluminous salvo of ‘I told you so’-esque journalistic put-downs of everything crypto, with every angle covered from the uninformed to the bizarre:

TL;DR

A mixture of regulatory worries, geopolitical tensions and general macroeconomic panic took Bitcoin down a peg from it's all-time high. Fraud numbers unveiled at the end of 2021 put new pressure on the government to regulate crypto, spreading fear through the market. Soon after, internet shutdowns amid protests in Kazakhstan sent the Bitcoin hash rate tumbling, again jolting markets with unpredictability. All this came amid a general market sentiment of uncertainty as the Fed’s December meeting notes indicated an eye to hiking rates periodically in coming months.

Despite getting its foot in the door of mainstream portfolios by being a hedge against the dollar and acting as a store-of-value, Bitcoin has rapidly become highly correlated with the S&P500. In previous bull runs, Bitcoin’s correlation coefficient with the S&P500 was 0.01, perfect for portfolio diversification. That number now sits at 0.36. Mainstream adoption may have caused a conflation of Bitcoin’s disruptive potential with being a ‘tech stock’ rather than a new kind of money.

Emerging Markets’ response to current macroeconomic uncertainty will be a moment of truth for Bitcoin’s proposition as a store-of-value. After the Fed’s December meeting notes, the IMF issued a warning to developing economies to be ready for capital exodus and depreciating currencies. How governments and citizens alike choose to protect their wealth will say a lot about just how seriously these nations take Bitcoin as a store-of-value. The non-speculative use cases and world-leading adoption of blockchain in many of these states says that there is a strong case they might provide a boon to prices as rising interest rates inject more negativity into traditional markets.

How Did We Get Here?

The opinion headlines above were all from the month of January, coincidentally coming after the fall in the price of Bitcoin. There a range of potential factors that could be attributed to catalysing the initial downward momentum on price, among them being:

Regulatory Worries. It’s hard to think it was only 3 months ago that a16z got on the front foot and published ‘How to Win the Future’, their comprehensive policy guide for web3 that sought to work in collaboration with the government to ensure that the ecosystem was responsibly regulated. Oh, how things change (or just get ignored).

On Jan. 27th, the Biden White House said that they would review treating cryptocurrencies as a matter of national security. Outside of the US, proposed and enacted bans in Russia and China respectively have not only shown the ease at which the market can be cut off, but also serve to limit the total market size of crypto applications.

One can see where that conclusion might’ve been reached - at the end of last year, much was made in the press about the record volumes of crypto fraud in 2021 (~US$14bn). While there are some caveats to this figure, not least the fact that scam revenue was inflated by the tremendous appreciation of cryptocurrencies in 2021, the figure brings to attention the non-price risks associated with crypto assets, something that is unlikely to make institutional or retail investors feel more comfortable with their holdings.

Kazakhstan. Whilst likely not the biggest driver in the price collapse, Kazakhstan’s close ties to the crypto ecosystem and the timing of major political events in the West Asian nation make its role interesting nonetheless.

Credit: Kazakhstan On Jan. 2nd, protests broke out across the country over the government’s raising of the price cap on LPG, pretty much doubling average fuel prices. Over the next couple of weeks, Russian troops got involved and there was a prolonged internet shutdown. This second bit is important - when China imposed their ban on crypto last year, several large mining operations in the country’s North decided to relocate to Kazakhstan, bestowing upon it the honour of becoming the world’s 2nd largest bitcoin mining hub. So, when the internet was cut out in Kazakhstan, Bitcoin’s hash rate declined 12%.

Theoretically speaking, this shouldn’t have sparked a decline in Bitcoin value - a lowered hash rate translates to decreased expected money supply, which would logically be inflationary. But we don’t live in a world of theory.

Coincidental or not, the timing of the social & functional unrest in the country is pretty closely lined up to Bitcoin’s decline, suggesting the possibility of panic sell-offs.

Interest Rate Panic. This is where things begin to get interesting and start hinting towards a paradigm shift in the way the market approaches Bitcoin. After a golden 24 months of stimulus, low rates and money printer brrr’ing, the Federal Reserve’s meeting minutes for December presented a return to more conservative measures.

The big news was absurd annual CPI inflation of 7% and a tight labour market amidst the ‘Great Resignation’. The solution? Sooner-than-expected rate hikes. As a wise woman (Nelly Furtado) once put it: “All good things come to an end”.

Nelly Furtado, crypto oracle. Source: @HashtagAlex There’s nothing unusual about this news triggering a slouch in the S&P 500, slowing economic growth by curbing investments in new projects or forcing investors to be more restrained in their decisions. It is, however, unusual that it would be so closely correlated to a decline in the value of Bitcoin.

There may be some low-level explanations for this correlation, like the large number of retail investors that have come on board in the last couple of years offloading these high-risk virtual assets to pay off very real debts that just got more expensive.

More likely is that Bitcoin and other virtual assets could have maybe just reached a level of mainstream awareness that has seen them cross the bridge from being a ludicrous impossibility to becoming a novelty asset. This newfound novelty may have seen it lumped in with the other novelties of the market - tech stocks.

Cyclical Issues. In Crypto, the term cycle gets thrown around a lot but not quite in the same way that it has been used in the macroeconomic discussions of old. This kind of cyclical thinking involves a healthy portion of bro-science and tends to centre around trying to time the market around approximately 4-year cycles.

Economically speaking, cycles tend to happen when there is inflation in the market (typically caused by excess demand) that at some point has to be curbed through regression to a newer, more affordable price level. In reference to the dot point above, low interest rates massively increased demand in the public and private equity markets alike, leading to frothy (over)valuations.

With a shift in interest rates comes a shift in perspective that says that current demand is no longer tenable, leading to shrinking valuations and sell-offs as the market adjusts. This is a perfectly reasonable explanation for declines in the S&P 500, but less so for crypto.

At some point in crypto’s recent bull run, the market seems to have decided that, somehow, fiat interest rates are now a non-price determinant of cryptocurrency demand. Why this is the case is the perplexing part of the equation - as an asset that was designed to escape the confines of traditional finance, interest rates unsurprisingly have little to do with transactions conducted in Bitcoin.

To refer back to the dot point above, it could well be the case that a rise in mainstream adoption has caused Bitcoin to leap across the canyon of ignorance into the same bucket as all other novel offerings on public exchanges - designation as a ‘tech stock’. There were some hints to this happening in the past year, with Coinbase’s IPO and the rumblings about Crypto ETFs being the two most prominent.

While these kinds of moves represent some form of mainstream acknowledgement, this lazy bundling treatment only serves to mislabel crypto and expose it to the same risks as the tech sector.

This is problematic because the missions, products & services and nature of the two could scarcely be more different. The conflation of the two represents an existential crisis for Bitcoin as it risks being misrepresented and misinterpreted among the masses, potentially corrupting the values at its core.

The Correlation Conundrum

From when the white paper was first penned in 2009, Bitcoin’s disciples have lauded the intrinsic value it derives from:

The ability to act as a deflationary store of value

Being an international and decentralised digital medium of exchange

Acting as a unit of account

Outside of the three words highlighted in blue, these cryptocurrency attributes are no different to the properties of old-fashioned fiat money.

The theory behind these points of value add is sound. Bitcoin is deflationary because of its capped supply of 21 million, with rewards for mining those remaining halving continuously. It is decentralised because of the proof-of-work consensus mechanism that Bitcoin employs relies on a network of validators instead of one central body like the Federal Reserve, and it is digital because, well, it exists in code.

In practice, at least in Bitcoin’s continuing infancy, this theory has been challenged. In the past year, mainstream adoption rapidly accelerated, not only through the introduction of crypto-based financial products like ETFs and company listings on regulated markets as previously mentioned but more importantly through the sheer number of everyday people that made the jump to owning some form of cryptocurrency.

If that trend in new wallet users isn’t stark enough evidence, 16% of American households claim to have invested in some form of cryptocurrency. While this may not sound like much in absolute terms, it is equivalent to every American over the age of 65 being a Bitcoin hodler and only 2% behind the proportion of American households that are married with kids.

The obvious implication of the massive number of retail investors apeing into Bitcoin is that, as in 2017 and 2019, upward price momentum has accelerated with the onboarding of new investors keen for a quick hit.

The issue of correlation is painted clearly in the data. In that period from 2017 to 2019, the average correlation coefficient between Bitcoin and the S&P 500 was 0.01. Today, that figure stands at 0.36.

This is disturbing for a number of reasons:

It tests the store of value theory.

It limits Bitcoin’s diversification value to mainstream portfolios.

It subjects the value of what is designed to be a decentralised money to decisions made by centralised bodies.

This presents a difficult conundrum. On the one hand, increasing mainstream adoption is essential to the crypto mission. Without users, the dream of a decentralised web is relatively pointless. However, with these new adopters comes the complications, misrepresentations and opportunistic behaviour that has, in essence, turned Bitcoin and its companions into a speculative tech stock rather than a new kind of financial system.

A Real-World Experiment

The Fed’s rate rises don’t just suck for Bitcoin and its new big tech cousins. On January 10th, the IMF issued a warning to emerging markets telling them what they likely already knew - that they needed to strap in for a rough ride.

The risks of these rate hikes in emerging markets are much similar to those faced in the US, but with the added complications of foreign exchange volatility, debts denominated in foreign currency (often USD) and the frightening prospect of massive shifts of wealth to safer jurisdictions.

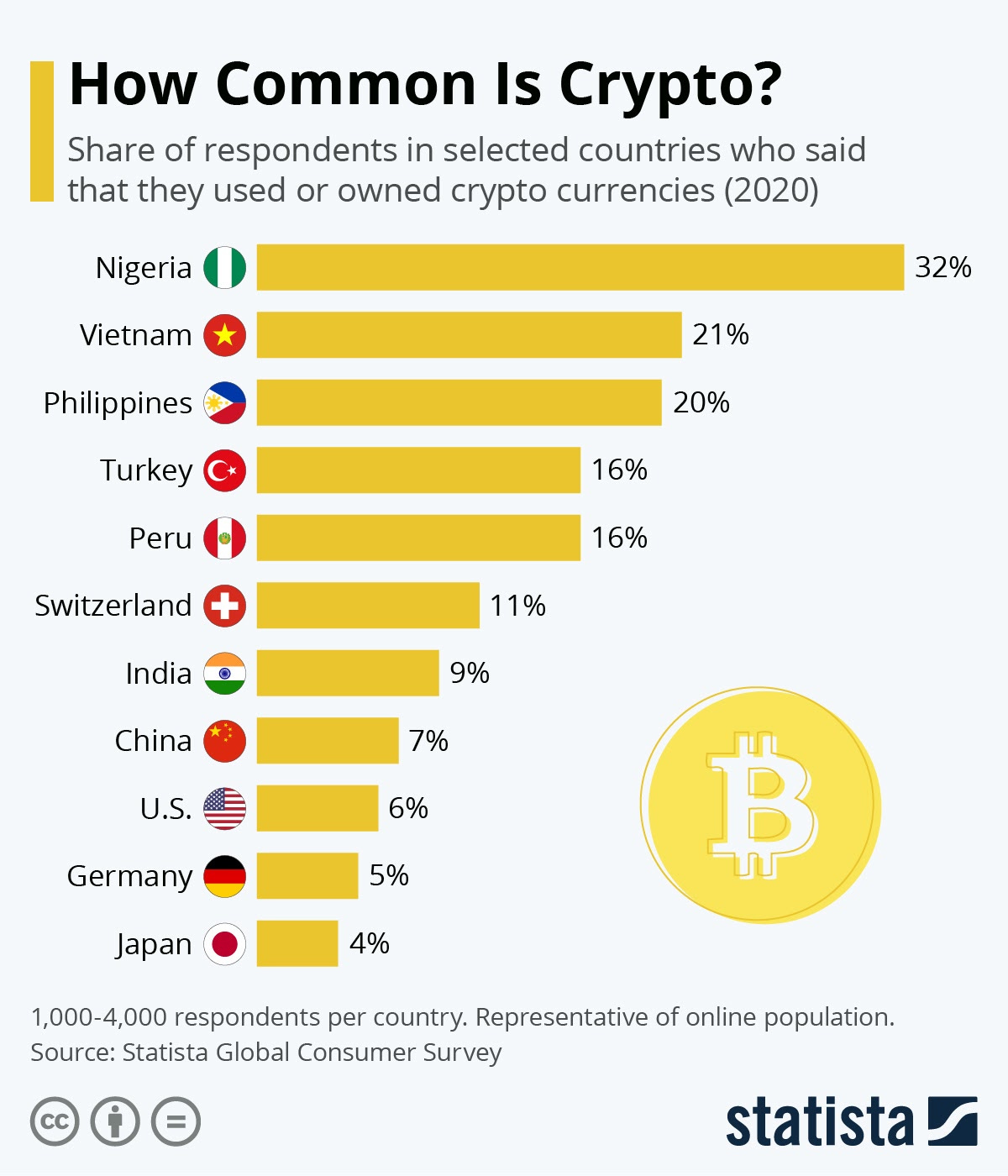

This last point is where Bitcoin comes back into the field of play. It’s been well publicised how much traction cryptocurrencies and blockchain applications more generally have received in emerging markets - based on adoption index scores developed by Chainalysis and the World Bank, 12 of the top 20 biggest adopters have come from the developing world.

Per capita statistics show a similar trend:

There are a number of reasons for crypto’s popularity in emerging economies:

Opportunity Value. Most developing countries are rife with financial issues. For starters, extreme wealth inequality is often a given. Currencies in many developing countries are unpredictable and weak against other common mediums of exchange.

Holding cryptocurrencies allows users in these countries to hedge against these local currency risks and pursue wealth creation opportunities that were not previously available to them. Even though Bitcoin has been highly volatile since its inception, the opportunity to own a hyper-growth asset like Bitcoin offers an unprecedented path to financial freedom and more.

Beyond speculative value, Bitcoin often acts as a bank account for those in unbanked or underbanked areas, which not only serves as a store of wealth but also a gateway to investment opportunities outside national borders.

Removal of the Need for Trusted Institutions. A large part of what drives the systemic financial inequalities in the developing world that was touched on above is corruption or incompetency in institutions or a complete lack of appropriate institutional oversight altogether.

By owning decentralised assets like Bitcoin that exist outside of the jurisdiction of such institutions, holders relieve themselves of the manifold associated risks, which can be as drastic as dispossession, bank account manipulation and much, much more.

Seamless Remittances. Bitcoin and its ilk blow incumbent remittance titans like Western Union and WorldRemit out of the water when it comes to sending and receiving money across borders because it can deliver the same value proposition whilst removing two of the barriers that are necessary for traditional remittance providers to survive - hefty service fees (to capture value) and lengthy processing times (for KYC/AML purposes and because of institutional difficulties with cross-border transfers).

Even amidst the prevailing ‘crypto crash’ many of these benefits will hold true - the capacity for crypto wallets to act as decentralised bank accounts, enable easy cross-border transactions and act as untouchable assets won’t be going away.

However, the tech stock conflation and associated volatility may cause a rethink in how Bitcoin is perceived in times of extreme financial uncertainty.

As mentioned above, until all 21 million Bitcoin are mined, price stability will remain a pipe dream. This might prove problematic for those in financially volatile states looking to find a hedge against the impending risks pointed out by the IMF. This is the moment of truth where Bitcoin’s claim to be a store-of-value will be tested.

If a Nigerian crypto-holder is worried about the potential for hyperinflation of the Naira as a result of these macroeconomic uncertainties and corrections, the store-of-value theory attests that Bitcoin would act as an effective hedge. This, in turn, would be expected to drive massive increases in demand for Bitcoin as wealth is transferred from fiat to Bitcoin.

However, the rising correlation with risky tech equities means that these users’ hard-earned dough might be just as well off losing money in ARK ETFs as it would in Bitcoin, provided that these losses are proportionally less than those faced if they had held it in cash.

This is where another conundrum lies and where Bitcoin’s popularity in the developing world will shine a light on whether it acts as a trusted store-of-value or not.

The institutional deficiencies highlighted above means that while these citizens may be just as poorly off buying US shares, they often simply can’t buy them. Which, in the case of emerging market currencies depreciating more than Bitcoin in this tantalising phase between planned hikes and enacted hikes (which is unlikely to be universally the case), would lead these users to transfer their wealth to ‘store-of-value’ cryptocurrencies.

Given the weight of the developing world in the crypto ecosystem, it is plausible that the sheer volume of demand could cause these currencies will trend in the opposite direction to Bitcoin.

This is an experiment that will play out in real-time as the Fed goes through its expected periodic rate rises over the next who-knows-how-long.

The conflation with its techy cousins has triggered a speculative rush of selling out of cryptocurrencies. There is every chance that those who most stand to benefit from the benefits of cryptocurrencies in underbanked nations will offset this by proving Bitcoin to be a store-of-value.

Closing Thoughts

For the uninitiated, the tweeter in the photo above is (believe it or not) not actually a McDonald’s employee. He is Nayib Bukele, the President and self-proclaimed ‘CEO’ of El Salvador.

On September 7th 2021, Bukele put his nation on the map and into the pages of newsletters around the world when he announced that El Salvador would become the first nation to accept Bitcoin as legal tender.

5 months in, the economics press and the IMF have sharpened their knives and begun declaring the move a failure. Headlines in Fortune declared that it was a ‘mess by every measure’, Futurism didn’t hold back any punches when it ran the sub-heading ‘Like Bitcoin Itself, El Salvador isn’t doing so hot right now’. Oh, and the IMF pleaded for Bukele to halt the experiment.

He declined.

The photo above was posted on the date that Bitcoin came within scratching distance of $35,000 from its annual high of over $67,000. It also came a day after El Salvador’s national treasury purchased 410 more Bitcoins for their war chest. The average investor would read that and cringe. Bukele opted instead to photoshop himself wearing a McDonald’s uniform to make light of the price drop.

Some may have issues with the optics of a man who is responsible for a nation’s economy unapologetically memeing about the detriment of his decision-making to the short-term health of the economy. The 80% of El Salvadorians who approve of Bukele as a leader, however, are not among that crowd.

Maybe Bukele’s meme is an attempt to take the edge off what are very serious circumstances for his country. However, more likely is that Bukele is thinking ahead of the curve. He knows what a lot of the media and institutions in the developed world seem to ignore when they attack him - even if the price continues to fall, the long-run benefits and short-run conveniences for his constituents are worth it.

Bukele knows that, like the rest of the emerging markets that adopt favourable stances towards innovative financial systems like crypto, that there is a range of previously unfathomable wealth creation & protection opportunities to be accessed, as well as protections against the global macroeconomic risks that these nations have been victims to with no input of their own.

In short, he knows that the decisions he is making just might lead to a better chance that ESGMI.